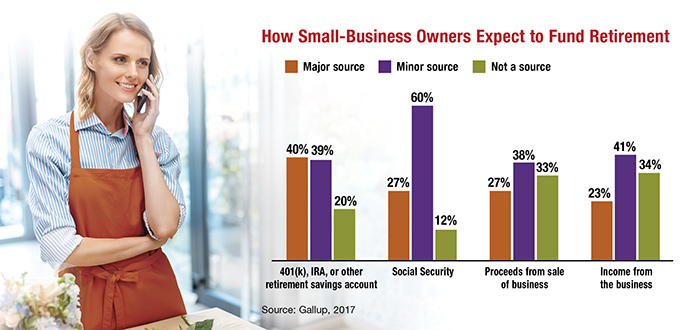

Working for Yourself? Don’t Sacrifice Your Retirement

Self-employment can be rewarding personally and financially, but it comes with some tough challenges including long hours, an uncertain income, and a lack of structured benefits such as health insurance and retirement plans.

But this is not the only reason it may be worthwhile to divert a sizable chunk of your earnings into tax-deferred retirement accounts. Doing so generally reduces your taxable income.

Anyone can set up an IRA, but contribution limits are relatively low — $5,500 in 2018, or $6,500 if you are 50 or older.

Here are two additional options that may allow larger contributions.

Solo 401(k). A solo 401(k) is a one-participant plan for business owners who have no other employees. Tax-deductible (or pre-tax) contributions to an individual 401(k) can be made in two ways.

As the employee, you can contribute as much as 100% of your annual compensation, up to the $18,500 annual maximum in 2018 ($24,500 if you are age 50 or older).

As the employer, you can also contribute an additional 20% of your earnings (25% if the business is incorporated) and deduct it as a business expense. Total contributions are capped at $55,000 in 2018 ($61,000 for those age 50 and older). A solo 401(k) plan may also allow plan loans and/or hardship withdrawals.

The deadline to establish an individual 401(k) and formally elect salary deferrals is December 31 of the year in which you want to receive the tax deduction (or before fiscal year-end for corporations). For businesses taxed as sole proprietors and partnerships, salary deferrals and profit-sharing contributions for 2018 must be deposited into the account by the April 2019 personal tax filing deadline.

SEP-IRA. You can make tax-deductible employer contributions of as much as 25% of net earnings, up to $55,000 in 2018. If you have eligible employees, you must contribute the same percentage to SEP-IRAs in their names; of course, the dollar amounts would be different for different salary levels. You are not required to contribute to a SEP-IRA every year.

In addition to any employer SEP-IRA contributions, you and your eligible workers can generally make pre-tax employee contributions up to the normal IRA contribution limits. You have until the April 2019 tax filing deadline to set up a SEP-IRA and make 2018 contributions.

Distributions from 401(k) plans and SEP-IRAs are taxed as ordinary income. Early withdrawals (prior to age 59) may be subject to a 10% federal income tax penalty.